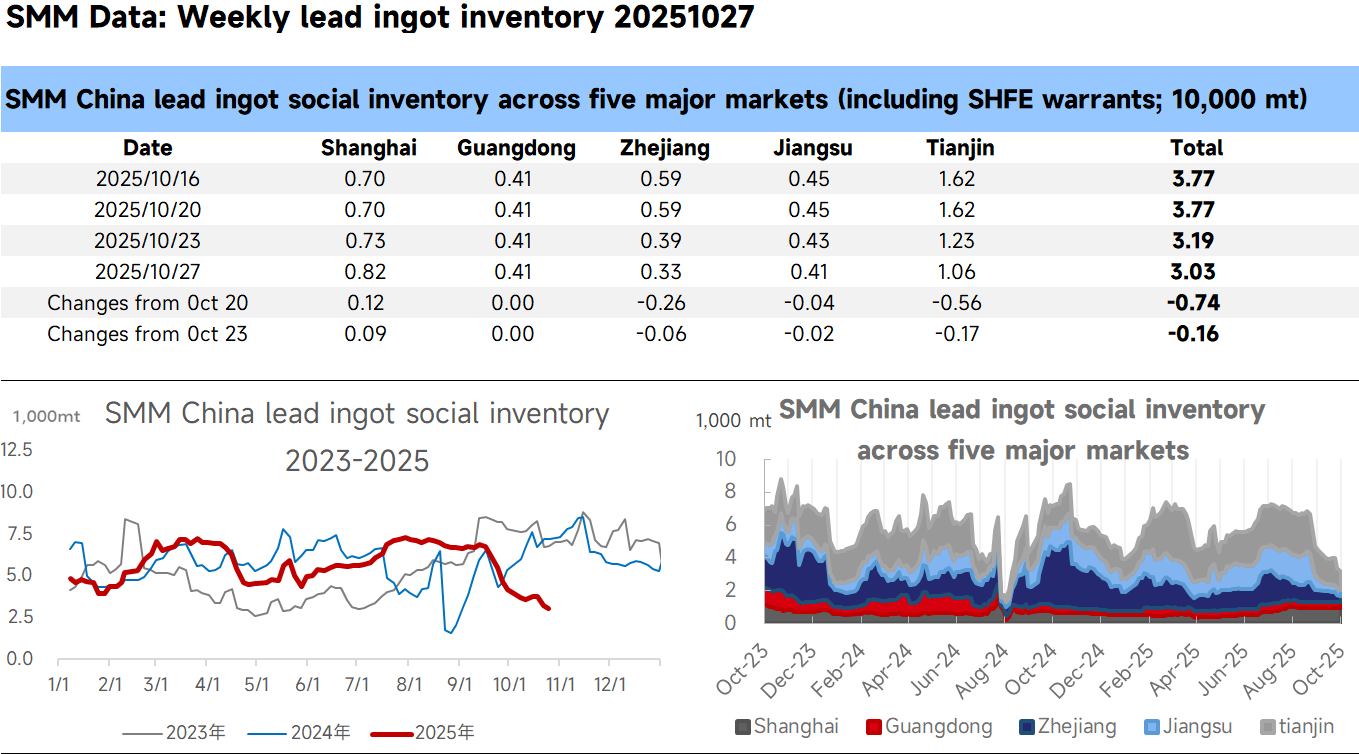

Following the sharp rise in lead prices last week, lead-acid battery companies significantly reduced their purchasing enthusiasm. In some regions, destocking at social warehouses has halted, with minor inventory buildup beginning. Meanwhile, primary lead smelters in North and Central China have not fully resumed operations after maintenance. Some smelters have already sold out their October lead ingot production, leading to continued tight supply in the short term. Social inventory in North China continued to decline, contributing to the overall decrease. Social inventory of lead ingots is expected to remain low until November. After November, attention should be paid to domestic suppliers shipping to delivery warehouses and the impact of imported lead arrivals on social inventory.

Data Source Statement: Except for publicly available information, other data are processed by SMM based on public information, market communication, and SMM’s internal database model. The data are for reference only and do not constitute decision-making advice.